CFA

CFA

CMA

CMA

ACCA

ACCA

初级会计职称

初级会计职称

CPA

CPA

-

在线咨询

-

官方热线

4008078199 -

APP下载

-

意见反馈

-

证书介绍

About The Certificate

ACCA 特许公认会计师公会

ACCA是特许公认会计师公会(The Associattion of Chartered Certified Accountants)的缩写,成立于1904年,是全球广受认可的国际专业会计师组织,是全世界有志投身于财会、金融以及管理领域人士的首选专业资格。

考试日历

季考

-

北京

北京

《在京发展的16项政策》 在京发展的16项政策中指出,加强对高端金融人才ACCA等在引进住房保障医疗健康,教育培训、子女入学等方面的服务。享有个人所得税优惠还可以办理调京手续办理本市户口,给予落户积分优惠。

-

上海

上海

《上海市重点领域 (金融类)“十四五”紧缺人才开发目录》 将ACCA人才列入“业务类金融紧缺人才”、“专业服务类金融紧缺人才”两项人才大类,共计10项人才子类并优先列入上海金才开发计划。其中ACCA人才在居留、出入境、工作许可证、落户、安居等方面获得更多支持以及便利优先推荐,同时还有参加上海金融人才实践基地实践锻炼和上海金融人才培训基地专题培训等一系列激励措施。

-

广州

广州

《2017年广州市高层次金融人才目录》 2017年广州在《2017年广州市高层次金融人才目录》中也明确将ACCA持证人列为行业研究人才,可参与高层次金融人才评定。被评定为高层次金融人才的ACCA持证人可以享受广州市政府提供的现金和一次性安家补贴,具体数额为最高不超过100万元还可以优先参加由广州市组织的赴纽约、伦敦、新加坡等地学习培训活动,在落户手续上,高层次金融人才可享受优先办理。 ACCA被列入广州市南沙新区重点产业急需人才名单。

-

深圳

深圳

《深圳市罗湖区高层次产业人才“菁英计划”、“福田英才荟”计划》 深圳罗湖区于2016将同时满足其他附加条件的ACCA持证人认定为B类“菁英人才”,可以一次性获得安家补贴30万元。另有住房优惠,子女入学优惠,健康管理养老服务等一系列福利。 深圳市“福田英才荟”计划 对获得特许公认会计师(ACCA)资格证书申报时未认定为深圳市高层次人才或孔雀人才,且在同一家辖区金融机构或金融专业服务机构从事相关专业工作连续三年以上的金融持证人才,给予一次性30,000元人才奖励。

-

杭州

杭州

《人才引进计划》 本科学历的ACCA持证人交满连续一年社保后就可申请落户。在省内事务所工作满三年期间,未受任何处罚考取ACCA等相关境外资格的奖励3,000元。

-

南京

南京

南京市人力资源和社会保障局发布了《南京市人才安居办法适用对象(目录)》。ACCA人才被列入南京市C、D、E类人才并可申请享受对应的安居补贴。 C类人才:获得ACCA资格、同时担任本市指定机构的高级管理人员,且申报时已在所聘任机构担任高管满3年的人才。 D类人才:获得ACCA资格、担任本市指定机构中层以上职务,已在所聘任机构工作满3年且申报时合同存续期3年(含)以上的人才。 E类人才:获得ACCA资格、年龄不超过45周岁、已在所聘任机构工作满1年且自申报之日起与所在金融机构合同存续期3年(含)以上的人才。

-

武汉

武汉

《市人民政府关于印发武汉市加快区域金融中心建设若干支持政策的通知》 武汉市自2021年6月30日起执行《市人民政府关于印发武汉市加快区域金融中心建设若干支持政策的通知》 ,对取得特许金融分析师(CFA)、金融风险管理师(FRM)、北美精算师(ASA)、中国精算师(FCAA)、英国特许注册会计师(ACCA)执业资格证书后在我市金融系统全职工作满2年的,按照每人2万元的标准给予一次性奖励。

-

青岛

青岛

《关于开展2020年青岛市金融高端人才推荐工作的通知》 2020年青岛市金融办发布《关于开展2020年青岛市金融高端人才推荐工作的通知》,ACCA证书持有者被纳入青岛市金融高端人才,可办理青岛市高层次人才服务绿卡,享受相关待遇,并最高享20万元补贴。

*资料来源:各省市人力资源和社会保障局及政府公开信息目录

ACCA助你不出国门便可获得三张海外名校学历+四张高含金量职业证书

牛津布鲁克斯大学应用会计(荣誉)学士学位

牛津布鲁克斯大学MBA

伦敦大学专业会计硕士学位

牛津布鲁克斯大学 Oxford Brookes University(OBU)

OBU国际大学排名超过中央财经大学、武汉大学等中国高等教育院校,OBU商学院拥有AMBA(英国工商管理硕士协会,世界三大商学院教育认证组织之一)认证,享有国际声誉。应用会计学是OBU的强势学科,处于世界领先地位,甚至欧洲大部分企业认为OBU毕业生与哈佛、耶鲁、剑桥、牛津等世界商科学府的毕业生齐名。

2022QS世界排名位居全球第429位(参考:中国排名第22位的上海大学位居全球第436位)

英国伦敦大学 University of London(UOL)

英国伦敦大学是由十几所英国高等学府和研究所组成的大学联邦,拥有英国皇家特许状,是全球颇具影响力的公立大学系统之一。UOL旗下的高等学府包括:伦敦国王学院、伦敦商学院、伦敦政治经济学院和伦敦大学学院等。

2022QS世界排名位居全球第8位(中国排名第1位的清华大学位居全球第17位)

商业会计证书

完成 BT-FA(前三门),并且通过基础阶段道德测试,即可获得。

高级商业会计证书

完成 BT-FM(前九门) ,并且完成道德测试模块,即可获得。如全部免试将无法获得此证书

ACCA准会员证书

13门科目全部通过即可获得

ACCA Member

通过13门科目后,累计三年工作经验,即可申请转为正式ACCA member。

无限职业可能

ACCA在全球的认可雇主企业已超过7500家,覆盖事务所、金融服务、科技等热门行业,从商业、电影、旅游到太空研究,为您打开精彩的职业大门

73%的受访企业高层都拥有ACCA会员身份(2018年雇主调查中显示)

60%的雇主希望聘请ACCA会员(2018年雇主调查中显示)

ACCA会员职位分布

OCCUPATION DISTRIBUTION

ACCA被誉为全球会计师的金饭碗,ACCA会员资格在国际上也得到广泛认可,他们大都在工商企业财务部门、(四大)审计/会计师事务所、金融机构和财政、税务部门从事高级财务管理工作,因此他们的薪资较普通财务人士普遍较高。

根据ACCA官方统计,中国ACCA会员有30%-40%就职于全球“四大”会计师事务所及中国知名会计事务所;40%左右就职于世界500强企业;另有30%左右出国深造。其会员目前在中国年薪分布在30-200万不等。21%的会员平均年收入在50-100万元,部分会员年收入高达200万元!

以下是ACCA在《首席财务官领导力调查结果》报告中关于480多位受访者的职位分布图

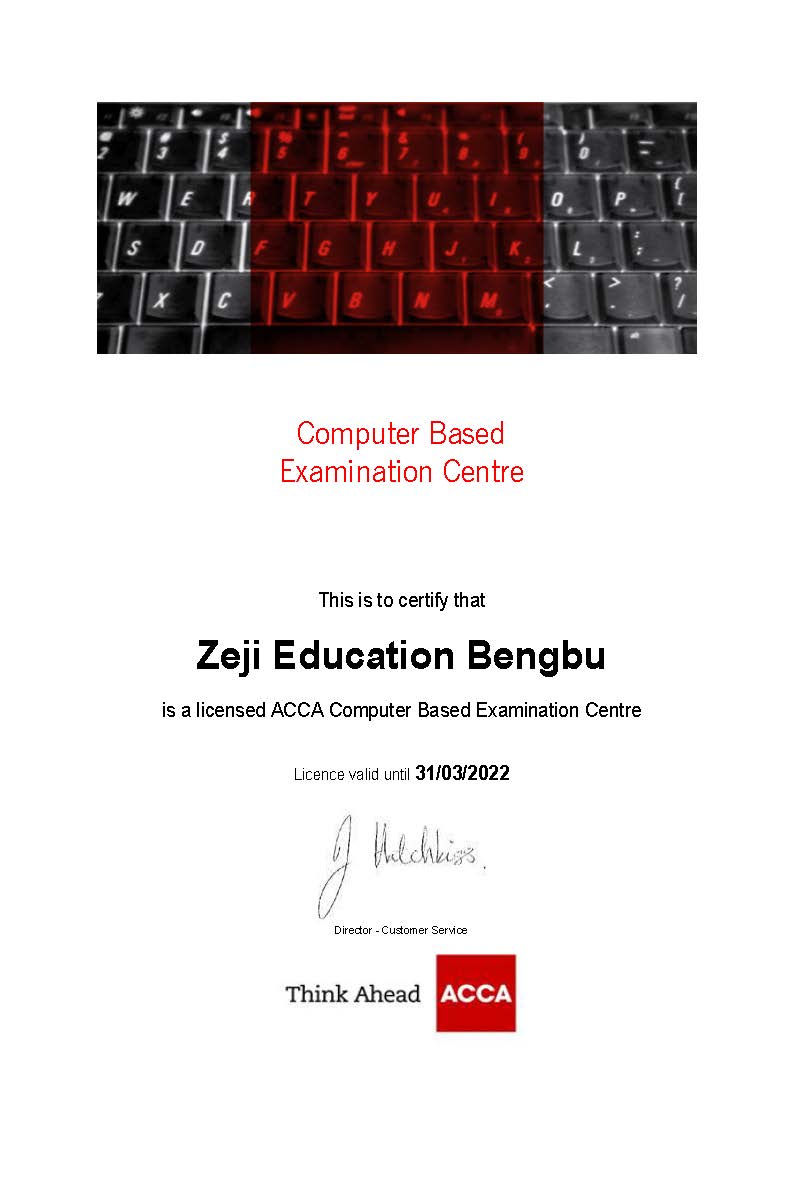

ACCA 机考中心

ACCA Computer Test Center

课程中心

Course Center

MORE +

-

ACCA 13门全科签约班 名师授课,全科高清网课+OBU论文申请辅导网课

ACCA 13门全科签约班 名师授课,全科高清网课+OBU论文申请辅导网课 6429

-

ACCA Pro计划之----尊享取证班 春秋季周末面授+寒暑假集训面授+在线私播+高清网课,多种学习模式,畅学5年学籍

ACCA Pro计划之----尊享取证班 春秋季周末面授+寒暑假集训面授+在线私播+高清网课,多种学习模式,畅学5年学籍 350

-

ACCA全额奖学金通关班 13科高清网络课程,通关即返培训费

ACCA全额奖学金通关班 13科高清网络课程,通关即返培训费 1699

-

ACCA Pro计划之----精品取证班 6科春秋季周末面授+13科寒暑假集训面授+7科在线私播+13科高清网课多种学习模式,畅学5年学籍

ACCA Pro计划之----精品取证班 6科春秋季周末面授+13科寒暑假集训面授+7科在线私播+13科高清网课多种学习模式,畅学5年学籍 167

-

ACCA BT - FA初级入门小白班 BT(F1) - FA(F3)初级入门高清网课

ACCA BT - FA初级入门小白班 BT(F1) - FA(F3)初级入门高清网课 4097

-

ACCA Pro计划之----无忧取证班 4科春秋季周末面授+13科寒暑假集训面授+9科在线私播+13科高清网课多种学习模式,畅学5年学籍

ACCA Pro计划之----无忧取证班 4科春秋季周末面授+13科寒暑假集训面授+9科在线私播+13科高清网课多种学习模式,畅学5年学籍 164

泽稷ACCA名师阵容

平均5-10年授课经验,曾就职于全球500强、四大等顶级企业。潜心研究教学内容,深耕ACCA领域,将实践教学与技能考试相结合,辅导出多名ACCA大陆第一及全球第一的学员,助力泽稷学员圆梦财经。Crystal Hu

泽稷国际会计研究院院长 ACCA首席讲师、辅导出多名ACCA大陆第一学员 被誉为“全科女神”

特许公认会计师公会会员ACCA、CMA持证人 伦敦大学会计学硕士 上海财经大学MBA 牛津布鲁克斯大学注册论文导师 拥有ACCA十年+教学经验,授课严谨,用其丰富的学识循循善诱,善于激发引导学生,被誉为“全科女神” 拥有多年普华永道PwC、中国平安总部从事审计、财务分析经验

Tim Han

泽稷国际会计研究院副院长 FA科目100%通过率导师 "Tim Talk"系列王牌主持人 B站大UP 交大学霸男神

上海交通大学会计学学士、MPAcc(会计专业硕士) 拥有丰富的四大会计师事务所审计、税务咨询方向工作经验 在ACCA教学领域积累了丰富的经验,带领多位泽稷研究院ACCA讲师一起构建了体系完整、结构精密的FA教学体系,大大提升同学的通过率。 职业规划大师,曾帮助10000+学员完成职业规划,教学方法精准独到,授课风格幽默诙谐,人格魅力满分,多次被学生评选为深受喜欢的讲师,被誉为“交大学霸男神”。

Yvette Zheng

ACCA资深讲师 辅导出ACCA全球第一学员,有“学霸型导师”之称

特许公认会计师公会资深会员FCCA 新加坡注册会计师 牛津布鲁克斯大学一等荣誉学士学位 伦敦大学会计硕士 牛津布鲁克斯大学注册论文导师 ACCA book prize得主 ACCA考试中有11门科目取得新加坡前3,全球前15名的优异成绩,11次获得新加坡 ACCA prizewinner奖项,多年ACCA教学经验,被誉为“学霸型导师” 拥有丰富的国内外大型会计师事务所(KPMG、BDO)审计与咨询经验。

Larry Yu

ACCA资深讲师 多位全球第一&大陆第一考生授课讲师

国内某知名财经大学博士 扎实精深的专业知识背景 曾获中国大陆ACCA优秀专业指导教师称号,应邀到越南、马来西亚等国家分享教学经验。 常年担任ACCA官方特约讲师,教学方法精准独到,广受学员好评,分别辅导出了5名TX大陆第一考生以及2名TX全球第一考生!

Christina Zhu

ACCA明星讲师 TX科目教学带头人

特许公认会计师公会会员ACCA 澳洲注册会计师协会会员(CPAA) 麦考瑞大学专业会计硕士 霍尔姆斯学院MBA学位 曾任职于世界500强企业,从事财务及分析工作。兼备丰富的国外工作经验与扎实的理论知识背景,在财务及税法领域有丰富的教学经验擅长结合实例分析,对知识点精准把控,很好地解决考生的备考痛点,所教授学生保持较高通过率。

Xin Wen

财务会计界女神

特许公认会计师公会会员ACCA 先后任职于北美跨国企业和美国纽交所上市大型能源企业,多年从业经验,拥有丰富的财务分析与会计实操经验 擅长以理论联系实际的方式帮助学员掌握课程核心内容,直击考试重点,尤其擅长财务会计课程FA、FR、SBR,被誉为“财务会计界女神”

Aimee

FM科目教学带头人 ACCA高分速学引领者

多年财务管理课程教学经验,擅长用自己高分快速通过ACCA的学习经验教授学员,授课思路清晰,以高效简易的方式传达课程核心 多年高校职业规划讲座经验,曾为数千名学员提供职业规划指导,辅助学员斩获心仪offer

Yang Zeng

ACCA考霸男神

特许公认会计师公会会员ACCA,CFA会员 英国帝国理工学院经济学硕士,名副其实的“考霸男神” 先后就职于毕马威华振会计师事务所、英国大型能源公司及基金公司,拥有扎实的知识背景和丰富的审计、分析、金融相关工作经验。 授课范围广泛,注重增加同学实务知识与提高学生的应试技巧见长。

Frances Wang

ACCA资深讲师

特许公认会计师公会会员ACCA 十八年英国伦敦的生活与工作,积累了丰富的财务工作经验 十年+ACCA授课经验,具备深厚的教学底蕴,潜心研究ACCA考试体系与考试方向,深度把握考试脉搏。 授课风格深入浅出,逻辑清晰,教授出多科目数百名高分学员

Jasmine Liu

ACCA人气讲师 应试技巧先锋者

毕业于知名大学商学院 伦敦大学会计学硕士 曾先后供职于KPMG管理咨询部及知名金融机构投行事业部 具备扎实的项目投融资实践经验、财务报告分析经验及公司内部控制治理经验 课程培训经验丰富,对ACCA应试与培训颇具心得,以逻辑思维见长,教学思路清晰严谨。

Claire Luan

ACCA资深讲师

特许公认会计师公会会员ACCA 知名高校会计学硕士 英国会计师事务所五年的资深会计师工作经验,熟知英国税法及国际会计准则 近十年ACCA教学经验,主要教授课程为财务会计,财务管理以及英国税法,擅长结合自身工作经验和丰富的课外知识,解释复杂的知识点,教学方法独到,对于考点的把握精准到位

Rose Pan

ACCA超人气讲师

海外名校商学院MBA硕士 任职于大型医药公司财务经理岗位,具备多年相关工作经验, 对经济学与企业管理等领域课题有深入研究,课堂氛围饱含激情,教学方式别具一格,帮助同学迅速掌握知识点

Levana

ACCA方向班人气讲师 职业规划培训师

国内知名大学ACCA方向班 本科期间高分快速通过ACCA 曾供职于知名国企,拥有扎实的理论基础与全面的实操经验,善于利用自己学习ACCA积累的经验与方法指导学生,教学思路清晰,授课风格独树一帜,在泽稷教育与一众高校合作的方向班教学中备受追捧。 曾在多所一流高校进行职规培训讲座,培训逾千名学员

Frank Liu

ACCA资深讲师

知名985院校法学博士 法律知识专家 十年+的高校LW课程教学经验,为多所重点高校进行课程授课,曾教授出百余名高分学员 在教学活动中,丰富学生的法律见闻,结合时政热点有趣地解读生涩的法律知识,培养学员法律思维能力。

Ellen Ma

ACCA资深讲师

特许公认会计师公会会员ACCA CMA持证人 CICPA持证人 中央财经大学管理学硕士(会计学方向) 十年+高校财务管理课程培训经验,主讲ACCA MA、FM和AFM课程 2009年开始在全国多所重点高校和大型央企从事ACCA和CMA培训,其中包括武汉理工大学、浙江财经大学等高校以及工商银行总行、中国人保总公司、中国移动总公司等企业

Sally Liu

会计金融“双料学霸”

特许公认会计师公会会员ACCA 英国南安普顿大学硕士毕业,主攻会计与金融方向 曾就职于上海立信会计师事务所,通过国外深造与事务所的工作积累了丰富的财务知识和实务经验,在授课过程中完美地将理论与实践相结合,被誉为会计金融“双料学霸”。

Cheney Chen

ACCA人气讲师

国内知名大学会计学专业,本科期间高分通过ACCA考试 曾任职于中国铁建海外公司,多年丰富海外财务管理工作经验,熟悉法语区国家财务准则 对管理会计有自己的独到见解,授课风格幽默风趣,崇尚寓教于乐。

Amy Li

ACCA学霸型讲师 FA科目教学带头人

世界百强名校澳大利亚莫纳什大学金融学硕士 拥有多年大型国有银行金融理财部及会计师事务所的工作经历 丰富全面的金融及财会实务工作经验 善于帮助学生建立逻辑思维,提高分析能力 多利用案例、场景讲解知识点,传授课本知识的同时,培养了学员综合能力。

Kelly Liu

ACCA人气讲师

特许公认会计师公会会员ACCA ,CICPA持证人,CMA持证人 就职于大型国有企业,拥有丰富的总账会计工作经验 曾在伦敦会计学院中国代表处,国内各大财经院校教授近10门ACCA课程,贯穿ACCA全科教学,对考试大纲与命题规律有精准的把控。

Cassie Xie

ACCA资深讲师

特许公认会计师公会会员ACCA 拥有大型上市公司财务分析工作经验,在企业财务报表编制和财务分析方面具备丰富的实战经验 多年ACCA全职讲师经验,曾多次带出高分学员,所带班级通过率常年高于全球平均通过率 善于总结课程的重难点,讲课条理清晰,擅长运用生活案例,将抽象的理论知识与实际例子相结合。

Micky

ACCA资深讲师

特许公认会计师公会准会员ACCA 曾就职于BDO立信会计师事务所、瑞华会计师事务所等国内大型内资所 多次参与IPO项目审计和大型上市公司并购审计及年报审计,拥有丰富的实践经验 擅长结构性教学,帮助学生理清学习中的难点痛点,让学习变得更加轻松高效

Wendy

ACCA新锐讲师 会计金融“双料学霸”

澳大利亚悉尼大学会计金融双专业硕士 曾于悉尼知名500强从事资产评估和财务分析工作 国内双一流高校财务会计、管理会计教学工作经验 丰富培训经验与扎实理论知识背景的完美结合,授课过程中善于开阔学生思路,调动学习热情和积极性。

Kirk Zhu

ACCA人气讲师 FA高通过率导师

本科学习期间短时间高分通过ACCA全科考试 先后就职于多家500强企业,拥有丰富的会计、审计、金融实操经验 授课逻辑清晰,重点突出,所教授学员中通过率极高 ,曾辅导学员FA获得99分高分

Dannille Liu

ACCA荣耀通关女侠 MA科目100%通过率导师

拥有十余年ACCA执教经验,就职于国内知名财务咨询公司 MA科目所教授的学员中多次取得100%通过率 在多年的教学中积累的丰富的授课和考试经验,专业基础扎实,教学内容结构主次分明,上课风格生动有趣,利用大量浅显易懂的案例,使入门学员能够更好的理解教学内容,深受学员喜爱,被誉为“ACCA荣耀通关女侠”

Michelle Liu

ACCA明星讲师

国内知名大学ACCA方向班 高分通过ACCA全科 曾就职于国内知名会计师事务所,参与大型国企、央企以及上市公司的年报审计与尽职调查审计 在授课过程中以扎实的理论功底和实务经验帮助学生迅速掌握知识点。

Chandler

ACCA新锐讲师

特许公认会计师公会会员ACCA CICPA持证人 曾就职于天职国际会计师事务所,拥有超过五年的审计工作经验 曾多次参与IPO项目审计和大型上市公司年报审计,理论知识扎实,实操经验丰富 擅长结合实践经验与经典案例,帮助学生搭建课程知识图谱,助力学员快速通关。

Janet

ACCA新锐讲师

世界百强名校英国诺丁汉大学会计与金融硕士 曾于英国创业公司从事财务会计相关工作,多年跨国审计经验 善用实战经验引导学员思考,授课逻辑清晰,亲和有感染力。

在泽稷学习是件轻松的事

丰富的学习工具 满足考生不同场景的备考需求筑梦未来 菁英荟萃

500强名师 职场极致体验领取资料包

Receive Study Kit- 财务英语入门

- 历年真题答案

- 考纲白皮书

- 考前冲刺资料

- 名师内部讲义

- 在线题库

姓名

手机号

验证码

获取验证码

邮箱

提交

教学一览

Teaching Pictures合作院校

Partner School-

上海财经大学商学院

-

上海财经大学经济学院

-

上海财经大学外国语学院

-

上海财经大学公共经济与管理学院

-

东南大学经济管理学院

-

湖南大学经济与贸易学院

-

湖南大学工商管理学院

-

中南大学商学院

-

上海大学法学院

-

上海大学社区学院

-

上海对外经贸大学会计学院

-

上海对外经贸大学会展与旅游学院

-

南京审计大学经济学院

-

浙江财经大学工商管理学院

-

浙江财经大学数据科学学院

-

南京财经大学营销与物流管理学院

-

南京财经大学会计学院

-

南京财经大学食品科学与工程学院

-

南京财经大学管理科学与工程学院

-

南京财经大学工商管理学院

-

广东财经大学工商管理学院

-

广东财经大学法学院

-

浙江工商大学工商管理学院

-

安徽科技学院财经学院

-

安徽财经大学工商管理学院

-

江西财经大学工商管理学院

-

湖南工商大学外国语学院

-

上海商学院财金学院

-

上海商学院工商管理学院

-

上海商学院商务经济学院

-

上海商学院继续教育学院

-

湖南工商大学工商管理学院

-

广东金融学院工商管理学院

-

华东理工大学外国语学院

-

华东理工大学法学院

-

上海外国语大学国际金融贸易学院

-

东华大学旭日工商管理学院

-

广东工业大学管理学院

-

南京邮电大学经济学院

-

南京信息工程大学商学院

-

上海理工大学管理学院

-

上海海事大学经济管理学院

-

上海海事大学法学院

-

上海政法学院经济管理学院

-

上海电力大学经济与管理学院

-

南京工业大学经济与管理学院

-

浙江理工大学经济管理学院

-

上海海洋大学经济管理学院

-

广东外语外贸大学商学院

-

南通大学经济与管理学院

-

浙江财经大学东方学院工商管理学院

-

浙江农林大学文法学院

-

上海第二工业大学经济与管理学院

-

扬州大学商学院

-

泽稷网校公众号

-

泽稷网校微博

-

泽稷网校APP